The United States is the biggest consumer market in the world. It is also where ambitious international brands go to either scale properly or burn through seven figures frighteningly quickly.

US retail entry for international brands is not a growth tactic. It is not a box to tick once you have “done well in Europe”. It is a capital-heavy, operationally complex and strategically unforgiving expansion decision.

What struck me was not the size of the numbers. It was how disciplined the successful brands were compared to the ones that flamed out.

If you are considering US retail entry, this is what you need to understand before you sign a single distributor agreement.

Table of Contents

Introducing Tia

Tia Ellis is the CEO of Wildflower Insight and a leading expert in US retail strategy.

Over the past decade she has supported brands in generating more than $100 million in retail sales.

As a second-generation immigrant, she is particularly focused on helping founders decode the US system, from the distribution “chicken and egg” problem to navigating hidden retail fees and margin expectations that can derail a launch.

What’s Actually Working in US Retail Right Now

The “Hot” Categories

Walk any major US trade show and you will see waves of innovation clustered around a few themes.

Prebiotic sodas are everywhere. Brands trying to compete with Olipop and Poppi have flooded the category.

Plant-based continues to evolve beyond meat substitutes into functional ingredients, seaweed proteins and entirely new formats. Sustainability, clean labels and purpose-led positioning are now baseline expectations rather than differentiators.

If you are entering the US with “organic” alone as your hook, you are already behind. (This is not unique to the US by the way, as I made similar observations at Biofach the other week).

Viral vs Sustainable

Then there is the TikTok effect.

Remember the pickled garlic trend? A jar of garlic, shaken with sriracha and herbs, went viral. Retail shelves emptied faster than toilet paper in a pandemic. It tasted exactly as questionable as you would expect – but it sold.

The challenge for buyers with this kind of item is brutal. Is this just a two-week spike or a category shift? How can they possibly plan for this?

For founders, this creates risk on both sides. Under-produce and you miss the moment. Over-produce and you fund your own expiry chargebacks.

Realistically though, you can’t plan for that kind of viral moment – you have to stay true to your own path, and if one of your products happens to go viral, great, try to surf the wave…but you can’t plan for it.

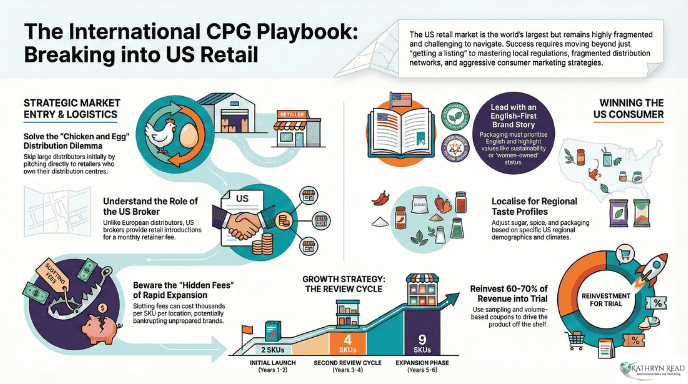

The Chicken and Egg of Distribution

This is where most international brands stall.

Retailers ask: who is your distributor?

Distributors ask: which retailer has listed you?

Nobody wants to hold the hot potato.

One workaround is counter-intuitive. Instead of chasing the biggest distributor first, focus on smaller retailers that allow direct delivery to their own distribution centres. Build proof of concept. Demonstrate velocity. Then turn that first account into a case study and use that to leverage your growth.

Once one retailer sees traction, others don’t want to be left out. Momentum in US retail is social (think peer pressure!) as much as commercial.

US Retail Broker vs Distributor for Food Brands

This is where terminology often trips people up and your FMCG expansion strategy needs to be very clear about which approach you need..

The Broker

The US retail broker model is largely unique: A broker owns the relationship with the retailer. They don’t buy your product. They don’t warehouse it. They charge a monthly retainer, typically between $5,000 and $10,000, to secure introductions and buyer meetings.

A good broker is worth their weight in gold. A vague contract isn’t worth the paper it’s written on, so make sure you have clarity.

Before signing anything, you should ask a potential broker the following questions regarding their fees and service expectations:

- What specific milestones does the retainer cover? You must clarify if the fee is simply for the “introduction” and “conversation” or if it includes securing a formal “buyer meeting”.

- What are the exact boundaries of your job description? Many founders experience failure with brokers because they do not clearly understand the broker’s specific responsibilities, so you must define these expectations upfront.

- Are there any “extra things” or discretionary fees I should expect? It is critical to ask about hidden fees or invoices that might appear later; the sources warn that “extra things” and discretionary chargebacks can cost a brand between $50,000 and $100,000, which can financially ruin a small company.

- Do you have existing relationships with my specific target retailers? Brokers often own relationships with specific retailers or categories, so you should ensure their current network aligns with the 5 to 10 specific accounts you are targeting.

- How will we manage financial transparency? You should insist on a clear breakdown of all finances before signing, as failing to ask deep questions about hidden fees is a common “key learning” from brands that struggled State side.

By asking these direct questions, you can avoid the “bad apples” in the industry and ensure your broker is a coachable partner who will help you reinvest your budget into driving actual in-store trials.

If you can’t define the deliverables in writing, you shouldn’t be putting all your hope in that broker.

The Distributor

In the US, large distributors are primarily logistics operators, who move product into retailer’s distribution centres. They do very little actual selling.

They usually won’t take you on without a retail commitment (that chicken & egg situation we mentioned before).

And here’s where the hidden costs surface.

Slotting fees (aka listing fees) can reach around $1,000 per SKU per distribution location. Nine SKUs across five locations quickly becomes a significant line item. If you then add performance chargebacks for expired stock and discretionary deductions, you can see how brands suddenly face $50,000 to $100,000 in unexpected costs.

International brands often make a second mistake. They sign exclusivity agreements with small distributors who only service ethnic or speciality stores. Yes, sales happen and revenue flows. But ultimately growth is capped… & you’re stuck – you can’t pivot into mainstream retail because you are contractually tied.

Don’t make the mistake of containing your growth in this way!

Internationally (e.g., in Europe or Asia), a distributor usually acts as both the sales team and the logistics provider – they purchase your product and sell it into their existing retail network.

Summary Comparison Table

| Feature | US Retail Broker | Large US Distributor |

|---|---|---|

| Main Goal | Secure buyer meetings and sales | Logistics and delivery to stores |

| Inventory | Never buys or holds your stock | Requires retail commitment to hold stock |

| Costs | Monthly retainer (5k−10k) | Slotting fees and chargebacks |

| Selling | Actively pitches to retailers | Does “very very little” selling |

To navigate this, you could bypass the middleman initially by focusing on retail accounts that allow you to deliver directly to their own distribution centers, creating a “success story” that later attracts larger distributors as mentioned above.

Who Should Not Attempt US Retail Entry Yet?

Bluntly speaking, not every brand is ready.

You should not be entering US retail if:

- You can’t comfortably fund at least 12 months of market development

- Your manufacturing capacity can’t scale quickly to six-figure unit volumes

- You are still refining product-market fit in your home market

- Your strategy relies on going viral rather than building repeat purchase

- You have not modelled slotting (listing) fees, chargebacks and sampling costs properly

The US rewards consistency and capital discipline, but equally it punishes underprepared optimism.

The Regulatory and Localisation Maze as part of the US retail entry for global brands

Navigating the regulatory landscape in the United States is one of the most significant hurdles for international CPG brands, as the country lacks a single, centralised regulatory body for food imports. Instead, compliance involves a complex mix of federal oversight, state-level laws, and even individual retailer standards.

Remember, compliance is the minimum requirement though so this alone won’t won’t create sales. Too many founders treat FDA approval as the milestone whereas it’s simply the entry ticket to be allowed to play.

The real commercial challenge is localisation, both in flavour and in narrative positioning.

Federal Oversight: FDA and USDA

Most food and beverage products fall under the jurisdiction of the FDA (Food and Drug Administration) or the USDA (U.S. Department of Agriculture). A common pitfall for foreign brands is failing to appoint a US agent, which is a mandatory requirement for international companies looking to import goods. Additionally, US ingredient restrictions are often completely different from those in other global markets; what is permitted in Europe or Asia may be restricted or banned in the US.

The Complexity of 50 States + FMCG market entry requirements

Beyond federal law, brands must navigate the specific regulations of 50 individual states. This is particularly critical for products in sensitive categories like hemp-based items, which may be legal in one state but strictly prohibited in another. If a brand enters through a port in a state where their product is restricted, or attempts to sell to a distribution facility supporting that state, it can lead to a “nightmare” scenario where they must backtrack and recover the product.

Packaging and Labeling Requirements

Packaging is not just a marketing tool but a critical regulatory component.

- English-First Packaging: The US consumer market requires packaging where English is the primary language, and the text must be clear and concise.

- Mandatory Attributes: Labels must meet strict FDA requirements, but they should also be leveraged to highlight claims such as “clean” or “organic” status.

- Certifications: If a brand qualifies, displaying attributes such as “women-owned“ can provide a competitive advantage, as US buyers and consumers often look for brands with a compelling social story or specific heritage.

Recipe Localisation

Localisation often requires physical changes to the product itself to meet US expectations. This may involve tweaking recipes (such as adjusting sugar or spice levels) to align with the regional taste profiles of the specific US pockets where your target demographics live.

Localisation is commercial & also “hyper-local” because the US is not ONE market. Taste profiles differ by region. eg Coconut water thrives in California, Florida and Hawaii but your tropical hydration strategy may fail in colder inland states.

Retailer-Specific Standards

Finally, it is important to realize that individual retailers often have their own specific standards that go beyond government regulations. Understanding these “pricing and margin expectations” and documentation requirements for each specific retailer is vital for a successful launch.

Beyond flavour, your story matters. Women-owned status, sustainability credentials and social impact messaging can influence purchasing decisions in crowded categories. A technically compliant product without a compelling narrative struggles to convert.

Getting Listed Is Not the Hard Part of US Retail Entry for International Brands

Many founders believe the listing is the victory moment.

It’s actually more like the first step in a 1000km journey….

Once on the shelf, you must create pull because retailers don’t market your product for you. If it doesn’t sell, it expires. And if it expires, you pay chargebacks.

One brand Tia worked with didn’t attempt a national rollout. They started with two SKUs in a handful of regional accounts -a physical trial of real cups with real conversations. For the first year, they reinvested roughly 70% of revenue into in-store sampling. Over six years, they expanded from two SKUs to nine, using hard velocity data from each category review to justify the next step. That discipline, not luck, created scale.

They didn’t chase 5,000 stores across the whole country on day one. Instead they built proof and rolled out step by step.

Avoiding the national rollout fantasy in your FMCG expansion strategy

The phrase “national rollout” may sound glorious and like a pinball machine going off if you ever won the jackpot.

A 5,000-store launch can require roughly 100,000 units within approx 4 weeks though. Can your factory deliver that? Can your cash flow finance it? Can your logistics manage it?

Scale without infrastructure is how brands implode because they have no idea what will work, or the systems in place to support that.

PRE LAUNCH BUDGET CHECKLIST

To successfully master how to get international CPG products into US retail, your budget must account for more than just shipping and manufacturing. Based on the insights from Tia Ellis, here is a comprehensive pre-launch budget checklist designed to ensure your brand is set up for sustainable growth rather than a short-term “transitional” sale.

1. Manufacturing & Logistics Strategy

High-Volume Production Reserve: Ensure you have the financial capacity to manufacture a “ballpark number” of 100,000 units within a four-week window to support a potential national rollout. If you can’t produce 100,000 units within four weeks without destabilising your existing markets, you are not ready for national scale.

State-Side Warehousing: Budget for US-based storage if you aren’t shipping directly to a retailer’s distribution center.

Fragmented Distribution Costs: Account for the logistics of getting products to various regional systems, as the US lacks a centralized grocery system.

2. Regulatory & Localization Compliance

US Agent Registration: Foreign brands are often required to register and pay for a US agent to oversee food imports.

FDA/USDA Labeling Overhaul: Budget for a packaging redesign that ensures English-first text and highlights key attributes like “clean labels” or “women-owned” status.

Recipe Tweak Reserve: Be prepared to fund minor recipe adjustments (sugar or spice levels) to meet regional US taste profiles.

3. The “Sales Team” & Entry Fees

Broker Retainers: A US broker typically charges a monthly retainer between $5,000 and $10,000 just to secure buyer meetings.

Slotting Fees: Budget approximately $1,000 per SKU, per distribution location. For a brand with 9 SKUs in 5 locations, this can quickly reach nearly $50,000 in upfront costs.

Slotting isn’t optional in most cases so you need to treat it as a marketing investment, not an unpleasant surprise.

Distributor Commissions: Account for the “pennies on the dollar” or flat commissions paid to distributors who manage the retail relationship.

4. Marketing: Getting Off the Shelf

Aggressive Marketing Reinvestment: Successful brands often reinvest 60% to 70% of their initial revenue back into marketing to drive trial.

In-Store Sampling Programs: Budget for physical sampling (staffing, supplies, and “sample cups”) to convert curious shoppers into buyers.

Digital ads won’t replace physical trial in grocery. Budget accordingly

Promotional Buy-Ins: Factor in the cost of BOGO (Buy One, Get One) deals or high-volume coupons that encourage a “three-unit spend” instead of just one.

5. The “Safety Net” for Hidden Costs

Chargeback Buffer: Set aside $50,000 to $100,000 for “discretionary fees” and chargebacks for expired or unsold products.

Education & Strategic Planning: Budget for specialized programs that provide the “pricing and margin expectations” specific to each US retailer so you aren’t surprised by the cost of entry.

Delegation & Virtual Assistance: Consider the cost of a Virtual Assistant to handle data research and calendar management, which saves the founder’s time for high-level empire building.

FAQs: How to get CPG Products into US Retail

How much does it cost to enter US retail?

Realistically, brands should expect six-figure upfront investment when accounting for slotting, sampling, broker retainers and chargeback buffers.

Do I need a US distributor to get into American grocery stores?

Not always initially. Some regional retailers allow direct delivery to their distribution centres, which can help you build proof of concept for your FMCG expansion strategy.

What is the difference between a US retail broker and distributor?

A broker manages retailer relationships and sales conversations. A distributor primarily manages logistics and inventory flow.

How long does it take to scale in US retail?

Successful brands often take several years to build from regional proof to broader national presence.

Watch the Full Discussion

In this episode of International Expansion Explained, Tia and I unpack:

- The distribution chicken and egg problem

- The real cost of slotting and chargebacks

- Why sampling still outperforms digital hype

- How brands scale from two SKUs to nine over six years

If you are actively planning US retail expansion, this conversation will save you expensive mistakes.

Reach out to Tia here:

LinkedIn: https://www.linkedin.com/in/tiaellis/

Website: https://www.wildflowerinsight.com/

Instagram: https://www.instagram.com/wildflowerinsight/

Building a Sustainable US Retail Entry Strategy

US retail entry for international brands is not about chasing the biggest distributor, landing the flashiest listing or announcing a national rollout on LinkedIn.

It is about building controlled, repeatable velocity.

The brands that succeed in the United States are rarely the ones making the most noise. They are the ones modelling slotting fees before they sign. They are the ones reinvesting aggressively into sampling. They are the ones who understand margin expectations, protect cash flow and expand store by store with data in hand.

If you cannot fund market development properly, if your manufacturing cannot scale without strain, or if your strategy relies on virality rather than repeat purchase, you are not ready yet.

And that is fine.

The US market rewards patience, structure and long-term thinking. It punishes undercapitalised optimism.

If you are serious about US retail entry for international brands, build your plan as if you intend to be there in ten years’ time. Because the brands that endure are not the fastest to launch. They are the most disciplined in how they grow.

Thinking that working with a consultant would accelerate your international expansion?

If you’d like to learn more about working with me for support on your internationalisation projects or personal export knowledge, you can book a 30 minute international clarity call here.

If you haven’t already signed up for my free e-book about how to select which international market to enter next, you can do so here, or using the form below.

If you enjoyed this content please share it on social media or recommend it to your network.

Pin this post for later!

Kathryn firmly believes that business is done between people, and therefore places her focus on building strong relationships that form a solid foundation for doing business.

When she's not travelling around the world, Kathryn enjoys playing clarinet in her town's wind orchestra or sharing her love of the outdoors with her Scout group.